For Shipowners, Brokers are the face of the insurance industry. By working directly with Shipowners, they understand how to place risk on best terms. The strength of a relationship determines the relative suitability of terms. The better the Broker understands the nuances of the Shipowners business, the better they can translate those needs to the market. ‘Relationships’ have therefore been a key point of differentiation for Brokers to date. This doesn’t just reflect an understanding of a Shipowners operations, but also that of an Insurer, as they act as an intermediary between the two. Using the scale of their organisation, individual specialisms, reputation, performance over time, and networks, Brokers have a lot of influence. With the current digital movement taking place in the market, Brokers are looking at ways to adapt and leverage digital tools that are changing the way Underwriters assess and monitor risk.

There are Brokers that have already started their digital journey and have positioned themselves to succeed in an evolving marketplace. Analytics platforms, such as Quest Marine, have been deployed to advance operations, adding value by drawing on big data to diversify services and develop new products. This approach has been recognised by the industry and is increasing in terms of adoption. It’s this approach that we should look to extrapolate, how does a deeper understanding of risk add-value to existing services, and what new products can a Broker deliver to a client?

As new technologies are used to assess risk, Shipowners will need to understand how this affects their cover, what they can do improve their risk profile and ensure the best terms. Brokers will need to service this new need and have access to the same behavioural insight that digital environments provide.

Placement in a new market

To understand how a Broker will evolve, we need to look at how the market they integrate with will change due to digitalisation. Digital platforms and the democratisation of data will lead to a three-tier model, with Insurers optimising resource around the complexity of risk.

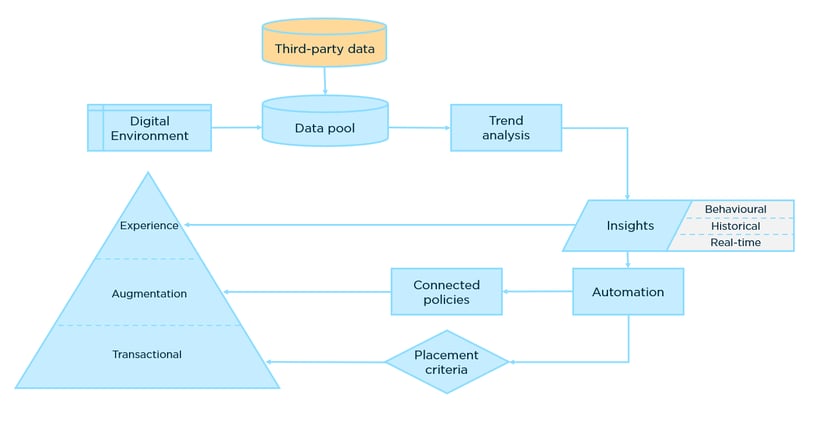

Fig 1: The adoption of a digital environment and its impact on placement, leading to a tiered approach

Fig 1: The adoption of a digital environment and its impact on placement, leading to a tiered approach

What we can see is that low value transactional business is automated. Augmented business will result in dynamic terms that are dependent on connected technologies, leading to connected policies. Complex risk will draw the most expertise and understanding to innovate and supply the market with bespoke products and services.

The impact of automation

Some speculate that automation will interfere with the current status quo, however it’s important to understand that automation will not undermine a Broker’s position. Direct-to-client markets that mirror consumer grade comparison websites won’t cater for complex needs. Looking at the new placement model (seen in Fig 1), those risks that require adaptive terms, or those that are significantly more complex will need just as much Shipowner representation as we see today.

It’s unlikely Broker profitability will be too heavily affected. The fact that automation makes transactional business both faster and more efficient can inflate the volume of business placed per period. Alternatively, if we base our assumptions of profitability and desirable business on transaction percentage, then the further up the tier we go, the more desirable the business becomes. High volume transactional business doesn’t rely heavily on a Brokers expertise as the risk profile is basic and simple to cover. The overall impact on Brokers can therefore be argued to be marginal and in fact gives the Broker back time to focus on more profitable business. Automation doesn’t negate the revenue opportunity from transactional business, as workflows can be set to give a Brokerage. Regardless, annual transactions as a focus are sunsetting in favour of long-term data-led services that are far more valuable to clients.

Data-led products and services

Understanding a Clients risk profile based on both static and behavioural data allows Brokers to better predict how Underwriters will determine the risk. This means that Brokers can better determine the Underwriters appetite and how it applies to market conditions. Further to that, risk profiles indicate which areas of a Shipowners operation carry the most risk. Brokers can utilise this information to advise on risk mitigation efforts, specifically where to prioritise investment and which behaviours to change. Successfully leading a Shipowner through such measures accelerates change and ensures best terms at renewal. This reinforces relationships with both the Shipowner and Underwriter. Underwriters specifically will acknowledge the fact the account is improving over time, and that the Broker is continually providing attractive business.

The ability to measure activity over the life of the policy provides Brokers with the opportunity to negotiate ‘connected policies,’ with terms that adapt to changing circumstances. If a vessel were to alter its activity for any reason, dynamic terms that depend on monitoring technology could ensure that cover changes as and when needed, protecting the Insurer and the Insured without punishing the Insured for what may be necessary behaviour. These connected policies are far more customer-centric when compared to static terms and ensure that Shipowners only pay for their usage.

With regards to highly complex risk, Brokers can generate reports and share their insight digitally or in person. Delivering such insight to those Underwriters that may not have fully invested in digital infrastructure doesn’t become a barrier to placing risk. When approaching Underwriters that have access to the same digital platform, such as Quest Marine, there is a shared view of risk. Therefore, bespoke products and terms can be created around account activity over time. This ensures that suitable cover is delivered to the direct needs of the Shipowner regardless of how unique their needs are.

A new business model

Adopting the very same technology Underwriters are using to better understand and monitor risk helps Brokers diversify and employ new capabilities to better serve the market. The nature of that market is changing around new ways to assess risk. Ensuring a Shipowner can gain a view of their risk profile, and know how to improve it, will be how Brokers add-value moving forward. Automation and advanced analytics have the potential to elevate what we see Brokers do in the market today, but through a business model based on consultation that is long-term and sustainable.

For more on how Broking will evolve through the influence of big data head over to our resource page, or how we can help your business, get in touch.