Read on to learn how exposure-based underwriting can lead to a new placement model for the cargo market.

Cargo is unique amongst the specialty lines. Unlike with hull or aviation, Underwriters and Exposure Managers have traditionally found it challenging to identify much about the specific asset(s) being covered. Vessels and aircraft can be tracked, their key features understood and claims resulting from physical damage investigated with relative accuracy. In cargo, beyond aggregate modelling related to catastrophe exposed warehouse locations and the vulnerability of cargo types, there has traditionally been no way of understanding where cargo is at any given point in time. Given the significant cargo losses that are often associated with natural catastrophe (Nat Cat) events such as Tjianjin, this poses a problem for exposure managers, increasing the potential for risk concentrations and “private catastrophe.”

Initiatives abound in response to this, incorporating everything from the use of sensor technology to monitor wine shipments, to the various blockchain consortiums seeking to leverage a real-time view of cargo transactions to track the flow of goods at the consignment level.

However, as is always the case, it is easy to get carried away with the destination, without a proper appreciation of the route to get there. Live tracking of cargo exposure is only one part of a patchwork of data, digital technologies, and services that (re)insurers will need to adopt in order to truly move to an exposure-based approach.

Step 1: Adopt a digital platform

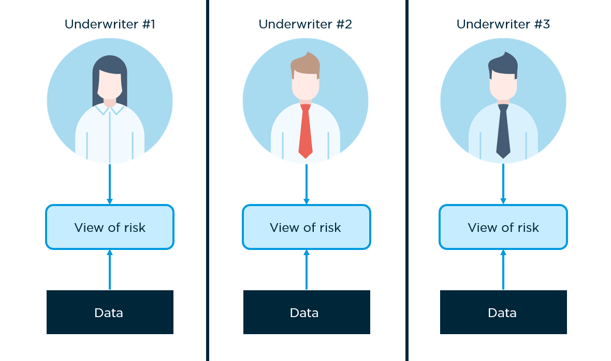

One of the biggest barriers we see to insurance companies reaping the benefits of the wealth of data now available on cargo, is fragmented storage of existing claims and exposure data. As well as being in multiple formats, it is spread across multiple systems with limited standardisation on how information is entered.

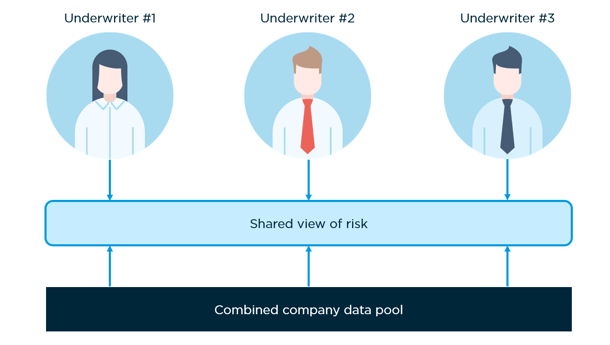

Drawing all exposure and claims data into a single digital environment provides a central resource to all teams. This immediately overcomes technological barriers to entry, such as file formats and competing systems. Visibility of data throughout the organisation is also democratised, ensuring all teams and staff have the same resource available to them.

Figure 1 & 2: A split organisational view vs a unified organisation view

Digital underwriting tools can be applied to the data in a single digital environment, uncovering new insights. This includes the identification of profitable routes, loss ratios across modes of transport, best/worst performing accounts, and the build-up of exposure geographically. When applied at account level, Underwriters can view a full account history as well as data-driven insights instantly. At portfolio level, exposure managers can drive increased segmentation analytics to identify previously unknown threats or opportunities. Such an understanding can resolve questions such as:

- What good types perform well and on what mode of transport?

- Is there a geographic imbalance to the portfolio?

- How is the loss ratio developing and in the aggregate are there attritional claims occurring in certain segments that are dampening performance?

Step 2: Incorporate third party risk data

With internal data digitised, there is an opportunity to supplement proprietary information and enrich the data pool. Validated external data, in conjunction with existing data, drives competitive advantage by building a broader vision of the market. It can expand exposure clarity, drive new insight, and improve the tracking of accumulations.

For example, rather than relying on submissions data, underwriters need only enter an account name to generate information on all exports and imports at the consignment level, per port, per day, along with associated values. This leads to a far more accurate view of exposure, leading to more informed decisions and better risk selection.

When integrated, exposure managers gain a rich view of portfolio accumulation. Instead of relying on traditional static modelling, underwriting can be correlated to the movement of assets, giving visibility around the build-up of risk in and out of ports globally. Stock throughput for different time periods can be calculated and storage location data incorporated to enable more accurate analyses of peak exposure and event losses.

There is however, no silver bullet for cargo exposure data and instead it is necessary to integrate multiple third party sources. Concirrus continually validates, aggregates and cleanses data from a range of sources to present the best coverage possible.

Step 3: Develop a new view of risk

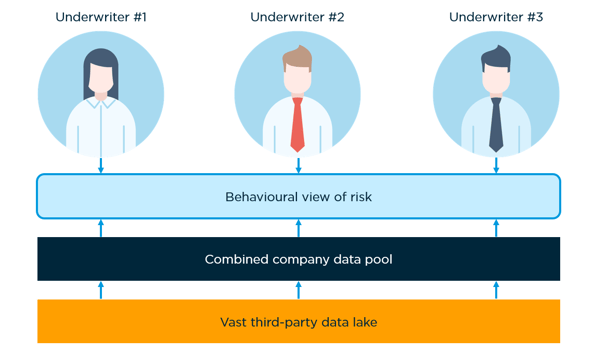

Once digitised in this way, machine learning can be applied to internal and third party data sets to identify correlations between cargo types, their movement and loss.

Figure 2: The application of a third-party data lake derives behavioural trends

Historical data gives the entire movement history of cargo for a client. It can highlight method, route, travel mix, issues and validate a hypothesis through catalogued claims.

Real-time tracking data completes the picture for an always-on view of risk. The combination of a digital environment that unifies proprietary, third-party, and real-time data provides a live view of transit exposure and accumulation.

These insights can be applied to build predictive pricing models, as well as enhance traditional catastrophe modelling workflows by driving clarity into exposure accumulations.

Step 4: Dynamic policies and increased automation

Once exposure visibility is established and accumulations are being actively managed, insurers can leverage the same technology, data and modelling techniques to properly integrate condition-based products as part of their offering. Without the necessary foundations, these initiatives struggle to scale and are difficult to manage within the context of a company’s legacy workflow.

Once a digital workflow has been established however, such “connected products,” can be distributed digitally, dynamically priced, automatically bound and actively managed using pre-defined triggers.

Indeed, it is arguable that if it’s possible to automate the process of condition-based policies, then it should be possible to drive increased automation in the more transactional segments of traditional cargo risk. Ultimately, this frees up the underwriter to deploy their significant experience and expertise to innovate and compete on complex risk at the top of the “placement pyramid.”

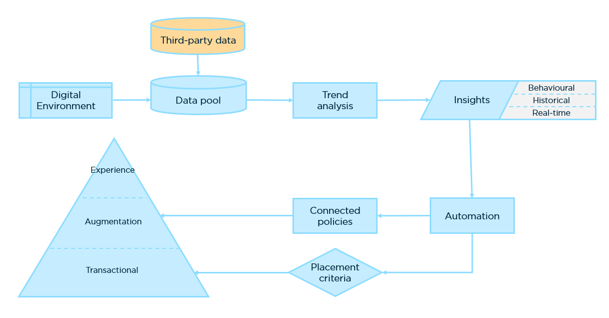

Figure 3: The digital journey to modern placement within the cargo market

In summary, whether the objective is to manage accumulations, improve pricing or launch innovative digital cargo products, it is necessary to take a holistic approach. As we have seen from our work with clients in other specialty lines, when done properly these initiatives can achieve real scale and deliver significant benefits to combined operating ratio (CoR). It all starts with building a digital foundation on your existing exposure and claims data.

To read more about how exposure-based underwriting can deliver a new placement model for the cargo market, download our whitepaper.