Learn more about the development of our predictive pricing capability within Quest Marine Hull and the opportunity it presents for the market in our blog 'How Predictive Pricing Can Enhance the Performance of the Marine Insurance Market'.

This blog was featured in IUMI's December 2019 newsletter.

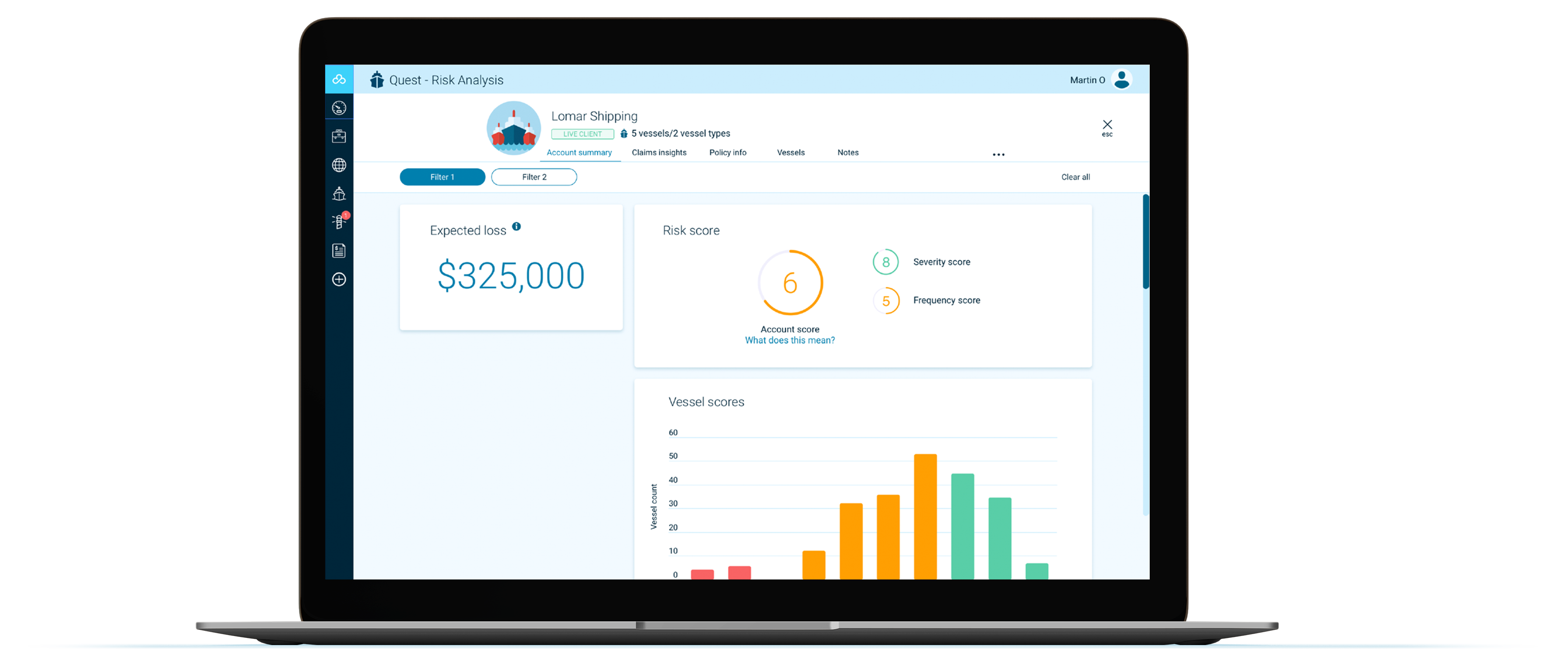

Digitisation is one of the most influential transformations taking place within insurance today. The development of a new predictive pricing capability within Quest Marine Hull highlights a move to further improve the accuracy of underwriting in the sector. The capability models both the frequency and severity of potential claims associated with an account. The result is an expected loss valuation with associated risk score that’s calculated using behavioural factors. This has the potential to drive multiple efficiencies within an organisation, as well as across the entire insurance value chain. Whilst the structure of the insurance industry will likely remain unchanged, the capabilities of industry experts will become far more advanced. Predictive modelling alone will provide a step-change for many within this space, allowing them to differentiate themselves in a highly competitive marketplace.

Advantages for Brokers

With an expected loss valuation and risk score, Brokers can better understand how they will be received by Underwriters before they meet. This ensures they’re more informed, know their walk away price ahead of meetings and are better placed to negotiate. If a score is adverse, the module will inform the Broker of which factors are impacting the valuation. Quest Marine Hull provides scores for an account, individual vessels within the account, as well as the most influential variables affecting account/vessel score. Brokers can use this data to consult a Client on where to direct investment so that efforts in improving risk management activities are reflected in total premium. Success will not only reinforce the relationship between the Broker and their Client, but also improve the quality of accounts the Broker takes to market. Over time, this will improve the reputation of the Broker in the marketplace.

Advantages for Actuaries

Actuaries typically create risk models manually. With the increasing volume and frequency of data received, they can become overwhelmed with the volume of information they have to process in a limited amount of time. Machine learning models within data aggregation software allows Actuaries to benefit from the automated interpretation of vast datasets. Actuaries can combine their expertise with the transparent view of risk modelling that Quest Marine Hull provides. This ensures that they can advise Underwriters and adhere to regulations. Results remain relevant due to the increased frequency with which modelling can take place.

.png?width=1440&name=Antilo%20Diagram%20-%20ML%20Approach%20(1).png)

Advantages for (Re)Insurers

An expected loss valuation for Underwriters enables them to better judge the relative premium they need to charge for writing risk. When combined with an associated score, the decision on whether to write the risk or not becomes even clearer.

An expected loss can also be used to calculate the effect of writing business on the portfolio. Doing so shows the impact of a decision on portfolio performance before it’s made. Underwriters can go into further detail on vessel score and influential factors to augment policies relative to each account and minimise exposure in specific scenarios. Head Underwriters can use the risk score to direct teams, setting thresholds whereby no business can be written below a certain score to help stabilise book health.

Digital tools also ensure there is no loss of information throughout the value chain. This ensures that an Underwriter has a complete view of risk regardless of the level of communication received from a Broker or other party. Even if there’s no existing relationship in place before doing business, there’s minimal degradation in data quality and understanding. This is also true when moving through to reinsurance.

Advantages for Capital

With improved performance of the value chain, loss ratios will become more stable and immediate rewards will be seen on the capital side. This makes the insurance industry more attractive for investment and encourages growth within the market.

Discover how we create predictive pricing models by clicking the link below.