Our latest pricing blog looks at how a suggested premium can be derived from an expected loss and applied to both new and existing business.

Quest Marine's pricing capabilities generate an expected loss for an account, providing a benchmark that underwriters can use when evaluating business. Influential factors demonstrate the reasoning behind such valuations, giving a new perspective on risk that may not be available through traditional means. The expected loss valuation can also be used to forecast a suggested premium for an account, creating a clear understanding of account value relative to organisational expenses and targets. This premium valuation adds perspective to both new and existing business.

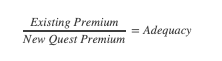

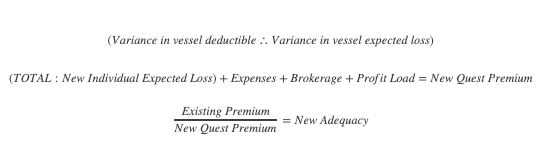

A forecast is conducted by utilising the expected loss of an account (net of deductible) and applying the brokerage, internal expenses, and profit load to derive a premium valuation. This premium is then compared to the written premium for the account to derive a percentage difference, known as the adequacy. The adequacy of an account will clearly show whether an account is technically under, or overpriced.

Utilising a generated premium and adequacy score provides a strong benchmark for underwriting teams to consider when writing or reviewing business. Hitting 100% adequacy ensures that all expenses and profit percentiles are achieved. Underwriters can use the adequacy score to ensure that their accounts hit a consistent threshold. The threshold is set through machine learning techniques derived from the organisation’s own claims data, making it pertinent to corporate performance. If the adequacy of an account is low, priorities can focus on increasing premium relative to risk. This can be done by identifying the vessels within the account that are contributing the most to the adequacy score and providing a measure of consultancy that leads to change. This will require consideration and agreement on both the underwriter’s and broker’s perspectives, allowing business to be written with securities in place. If above adequacy, then more favourable terms can reflect the attractiveness of the business as mentioned when discussing influential factors

Calculating the expected loss within the forecasting module at account level requires the deductibles per vessel be entered when creating a policy. An expected loss per vessel is calculated and the total of each sum is provided for the account. As the expected loss values at vessel level are net of deductible, the individual deductible valuations per vessel have a strong weighting on the outcome of the total expected loss figure for the account. Underwriters can test what variances to the deductible affects the expected loss of the vessel, and therefore the adequacy of an account, by editing the deductible valuations in a draft policy.

Simulating various deductibles can lead to optimised and targeted underwriting around existing valuations. Doing so directly improves the profitability of the account. If applied across the entire portfolio, it will give a measured and evidence-based approach to targeted performance.

For a detailed look at how this methodology is changing the industry, download the white paper or get In touch.