Global business leaders are assessing the full impact of COVID-19 with a focus on getting the economy back on track. Here we look at the latest global vessel movement trends to see if the shipping industry is showing signs of recovery.

May 2020 saw the following activity compared to 2019:

-

-

- A 10% global reduction in weekly distance travelled by containerships.

- Reductions in containership average weekly port visits across multiple regions.

- A 70.5% global reduction in distance travelled by cruise ships.

- Challenging risk aggregations of cruise ships in the Caribbean ahead of hurricane season.

- Changes to UCLV shipping routes as a result of significant reductions in oil prices.

-

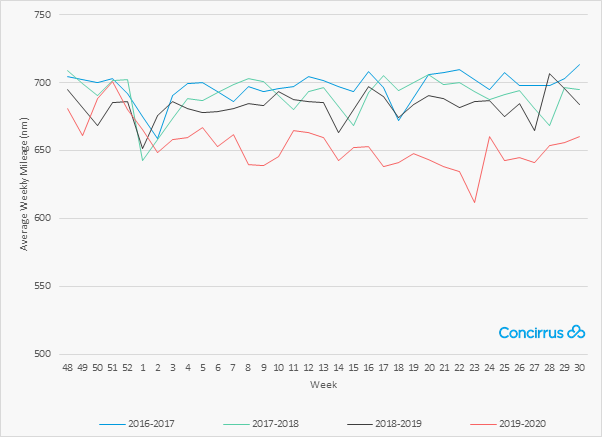

Three months on, global vessel data shows that average weekly mileage is increasing steadily.

Figure 1: Average weekly mileage – global, all vessels

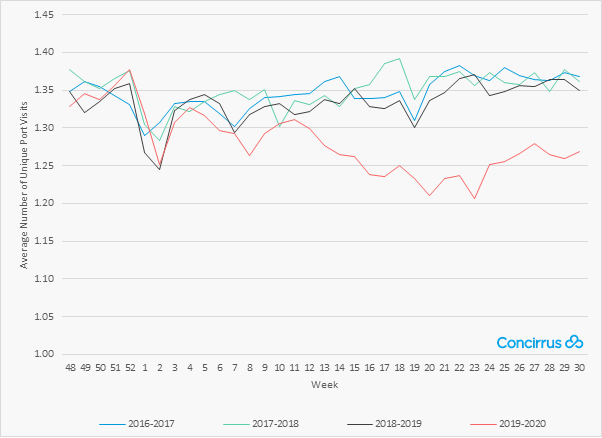

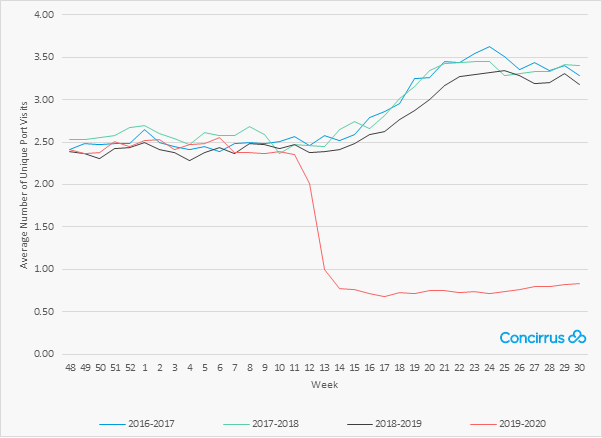

Global vessel mileage levels were down by just 3.5% vs 2019 at the end of July 2020. However, average weekly unique port visits have not yet stabilised at the same rate. During March 2020, average weekly port visits were 11.7% lower than in 2019. At the end of July, port activity still lagged by 5.9%.

Figure 2: Average weekly unique port visits – global, all vessels

Let’s take a closer look at port visit activity by vessel type and some of the regions most affected to understand the changing nature of marine risk within the sector.

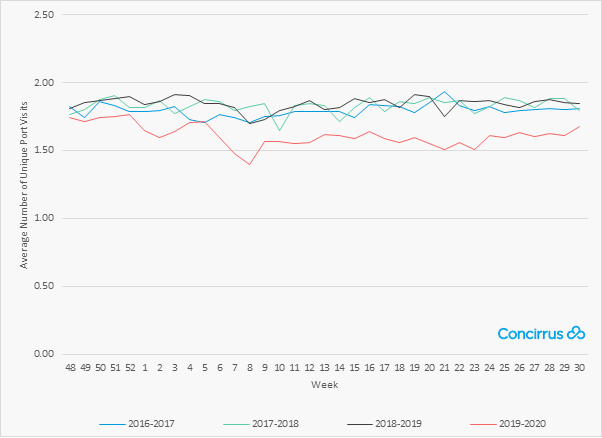

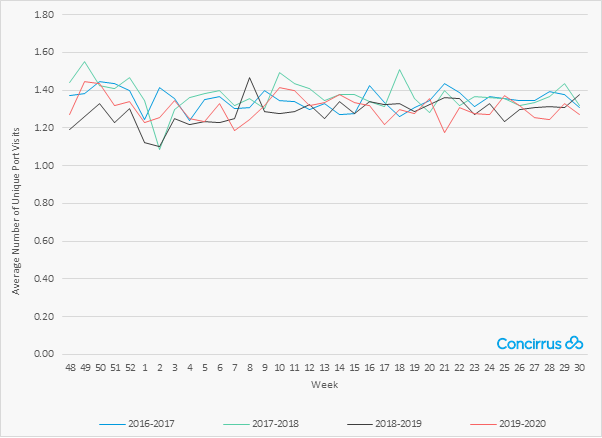

Average weekly unique port visits by region - containerships

A closer look at the data shows regional variations in containership average weekly unique port visits:

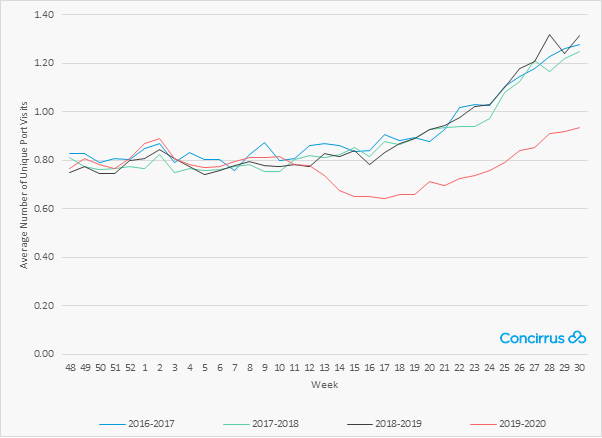

Asia

-

-

- A maximum reduction of 17.6% on 2019 average weekly port visit figures.

- July 2020 activity still lags 2019 by almost 10%.

-

Figure 3: Containership average weekly unique port visits – Asia

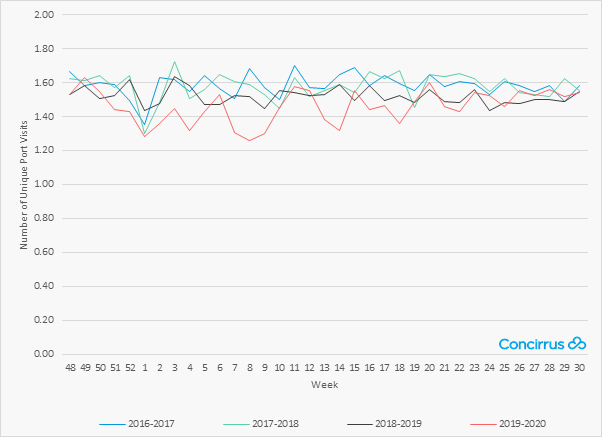

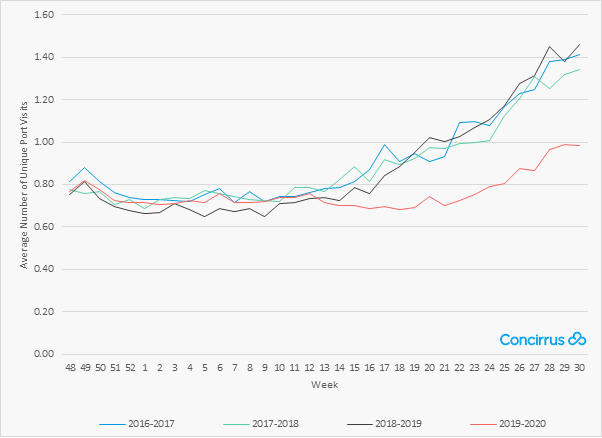

Europe

-

-

- A maximum reduction of 17.1% on 2019 average weekly port visit figures.

- July 2020 data shows activity has returned to 2019 levels.

-

Figure 4: Containership average weekly unique port visits – Europe

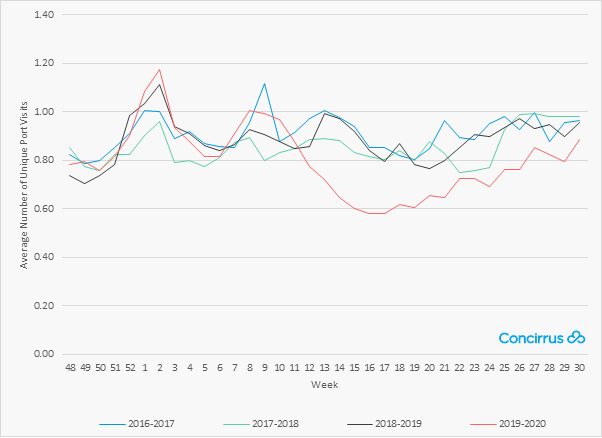

North America

-

-

- A reduction of 14% from 2019 for one week only.

-

Figure 5: Containership average weekly unique port visits – North America

South America

-

-

- Has shown no significant changes in 2020 compared to previous years.

-

Analysis shows that significant reductions in weekly port activity in Asia appear to contribute heavily to the global figures. Whilst Europe and North America have seen reductions on a similar level the changes have been limited to 1-2 weeks unlike the sustained reduction seen in Asia since March 2020. International trade has been restricted by COVID-19, global lockdown measures, reductions in retail activity and a turbulent trade relationship between the US and China, all of which could account for the sustained reductions in containership activity.

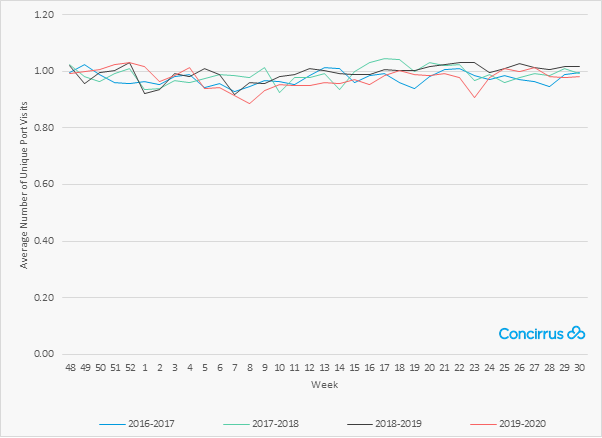

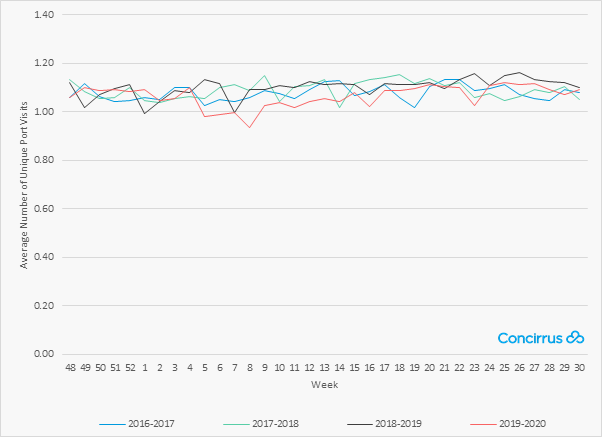

Average weekly unique port visits by region – bulk carriers

Bulk carriers have not experienced reductions like those in other areas during COVID-19. Their weekly average unique port visits have remained relatively consistent throughout 2020 when compared to previous years. At its lowest, weekly unique port visits reduced by 11.7% however the change was short-lived and activity levels returned to normal over the course of the next couple of weeks. A recent blog published by VesselsValue, Half Year Round Up – Trade, shows an increase in bulk carrier mileage and global trade from March 2020 compared to 2019 and suggests a positive outlook for bulk carriers.

Figure 6: Bulk carrier average weekly unique port visits – Global

Below we look at the regional variations:

Asia

-

-

- Week 8 saw weekly averages drop to 0.94, down 13.8% compared to 2019.

-

Figure 7: Bulk carrier average weekly unique port visits – Asia

Europe

-

-

- Reductions in activity are seen much later into the pandemic in Europe with weekly averages 13% below the same period in previous years.

- Fluctuations are much greater in this region and we can see reductions lasting for a period of 9 weeks.

-

Figure 8: Bulk carrier average weekly unique port visits – Europe

North America & South America

-

-

- Has seen no notable change in 2020 port activity compared to previous years.

-

Reports suggest that the demand for raw materials has remained consistent throughout 2020 with any regional reductions in activity being countered by increased supply and demand in other areas. The imposition of stricter regulations has resulted in a slowdown in construction which could see raw materials stockpiling in the short term in anticipation of increased levels of activity later in the year.

Average weekly unique port visits by region – cruise vessels

There has been a lot of coverage of the impact of COVID-19 on the cruise ship industry since March 2020. Global weekly average port visits were in line with previous years until week commencing 16 March when the industry came to a drastic halt. Due to the very nature of a cruise, weekly port visits were on average around 2.4 at the start of the year. By the end of March that figure was as low as 0.68, a reduction of 78.4% compared to 2019. And whilst there has been a slight increase in recent weeks the reduction in activity has been sustained over the past five months and there is a long way to go to get the industry back to normal trading patterns.

Regionally there’s not much variation, the trends for cruise vessels show consistent low levels of activity for most of 2020.

Figure 9: Cruise ship average weekly unique port visits – Global

Centers for Disease Control and Prevention (CDC) warnings currently stand at level 3 and recommend that travellers defer all cruise travel worldwide. With ongoing cases of the coronavirus disease documented across the globe and cruise passengers still at increased risk of person-to-person infection we can expect the industry to be one of the last to resume operations. Average weekly distance travelled dropped to an all time low in early July and the outlook for the remainder of 2020 is uncertain for this sector.

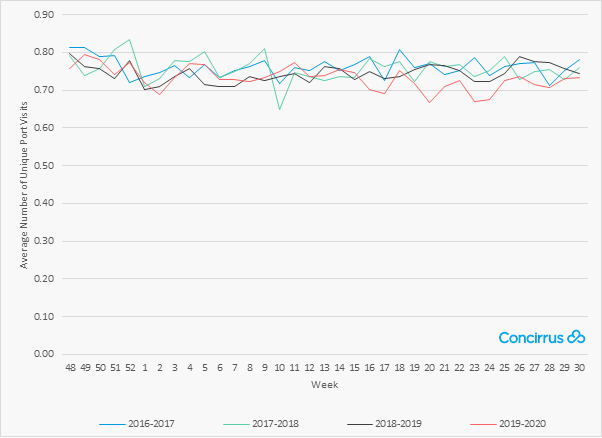

Average weekly unique port visits by region – yachts (+300 gross tonnes)

Historically, March has marked the beginning of a steady increase in the number of weekly port visits by yachts as the weather entices people onto the water throughout holiday season. However, COVID-19 and lock-down restrictions imposed during March has negatively impacted seasonal yachting activity. In mid-March 2020 we can see a clear drop off in weekly port visits for yachts across the globe.

Figure 10: Yacht average weekly unique port visits – Global

At its lowest, weekly average port visits by yachts reduced by 27.5% compared to previous year’s figures. Whilst activity is tracking historic trends the data shows that 2020 average weekly port visits since March lag previous years by a steady 25 percent to date. The most notable regional variations are shown below:

Asia

-

-

- 2020 vessel data shows no clear change compared to previous years.

- Port visits in this region have typically been very irregular throughout the year and 2020 follows a similar trend.

-

Europe

-

-

- Port activity has reduced significantly for yachts in this region compared to previous years.

- Weekly unique port visits dropped by 34.4% compared to the same time in 2019.

- In line with the global trends, we’re seeing activity increase but lagging previous year’s figures to date.

-

Figure 11: Yacht average weekly unique port visits – Europe

North America

-

-

- 2020 port visits dropped by 34.8% through March and April compared to previous years.

- Activity appears to be returning to previous levels in this region much quicker than in Europe.

-

Figure 12: Yacht average weekly unique port visits – North America

Yachting activities were initially impacted by strict global travel restrictions during lockdown. Once lockdown restrictions began to ease yachting activity has shown some signs of recovery. Despite a slight increase in the average weekly distance travelled and average weekly port visits neither are back to pre-COVID-19 levels indicating a cautious approach to vessel utilisation in the leisure sector.

What’s next?

It’s expected that port activity will continue to return towards normal levels as international trade resumes. However, as some ports are operating at reduced capacity, we could see a backlog of goods and therefore risk aggregations at key storage locations as smaller shore-side teams struggle to process larger volumes of cargo.

The cruise sector has seen the largest reduction in activity throughout the pandemic, yet is showing a slight increase in port visits in recent weeks. As we discussed earlier in this blog, average weekly distance travelled reduced by 70.5% and average weekly port visits by 78.4% compared to 2019 figures. The industry will be keen to welcome passengers back onboard as soon as possible and it is expected that vessels will be carrying out routine maintenance and relocating to passenger-onboarding ports prior to normal operations resuming. It will take some time for the cruise ship sector to return to normal operating levels due to extended restrictions and a reluctance from passengers to return.

Whilst global vessel data shows improvement, further analysis uncovers a variety of implications for specific sectors and regions. COVID-19, seasonal weather events, trade, oil prices, seafarer well-being, capacity restrictions and disastrous events such as the Beirut explosion continue to challenge the shipping industry. As the insurance industry works to effectively support their clients across the globe during the global pandemic, visibility of the variances in vessel types, regions and global benchmarks has never been more important. Armed with real-time visibility of emerging risks, detailed data and insights combined with internal expertise is a winning combination. It allows the insurance market to keep up to date with changing risk profiles and ensures that they can deliver risk management services tailored to their client’s situation. In a hard market competition is fierce and digitalisation of your data and processes can help you to differentiate your service and secure new business to grow your book.

If you would like to find out more about the breadth and depth of our data analysis, then register for the President’s Workshop at the upcoming IUMI annual conference on the 14 September. I look forward to sharing further insights with attendees in the workshop. Registration for the IUMI annual conference closes on Friday 4 September so register today.

Part one: 'Risk management strategies for shipping during a global pandemic'

Part two: 'Cruise ship risk aggregations in the Caribbean due to COVID-19'

Part three: 'COVID-19 and changes to containership (UCLV) mileage'