Last month we were thrilled to sponsor Marine Insurance London 2020 for the third year running. A key event in the calendar that brings the marine insurance community together. Cannon Events hosted the virtual conference and Mark Phillips, our Vice President & Head of Sales, presented his keynote address on how digitalisation is empowering the marine insurance community. Mark gave insight into the technology that is being adopted by key players within the market and how they’re using it to improve efficiency, reduce loss ratios and develop new products and services.

See the recording here.

Key challenges the marine insurance industry has faced in the last 12 months

The marine insurance market has continued to face the same challenge for many years; rates are improving across marine hull and cargo, yet the challenge of loss and expense ratios have remained ever-present. It’s this juxtaposition of potential growth on the one hand and poor returns on the other that is driving significant tech disruption across the industry as companies look to improve their position. 2020 was an interesting year for the insurance market. It marked a changing climate and COVID-19 altered the nature of risk, leading to an explosion of marine technology.

We’ve seen the rise of connected ships and the widespread use of cargo sensors. The incorporation of all this data along with new types of satellite information, real-time weather data, vessel and cargo positioning data is improving the efficiency and resilience of shipping and cargo operations across the world. Now that we’re operating in a changing climate that is increasing the frequency and severity of catastrophe events, we’re also seeing new trade routes emerge.

There’s one word that stands out which is ‘connected’. In this increasingly connected and dynamic world, the threats of the future are extremely hard to foresee. We hypothesise that the traditional approaches to risk rating (i.e. the static data assessments) that have been around for 100s of years are inadequate to deal with this increasingly dynamic and connected world. Without action and change, Insurers will continue to face the above challenges relating to loss ratios.

As always, the market is responding to the challenge of changing risk and digital. We’re seeing a whole range of new initiatives; the rise of connected products, countless digital cargo propositions based on sensor technology, an increasing use of sensors in hull policies, and automated war products. Data and digital technologies are enabling Insurers to respond, and they are reporting significant trading advantages.

Companies are incorporating sensor data with claims and exposure data to develop predictive loss analytics that improves their operations and pricing capabilities. There is also the notable rise of digital syndicates. The idea of using algorithmic pricing would have seemed incredibly far-fetched just a year ago. However, today we have key insures within the market using algorithmic pricing with almost $500 Million in capital behind it.

While these initiatives have pushed the agenda forward in 2020 and are undoubted to be applauded, what is the next step?

We see a bigger, more unique opportunity presenting itself. The launch of a comprehensive digital marine proposition that takes advantage of these trends.

What does this new insurance operating model look like and what technologies are required?

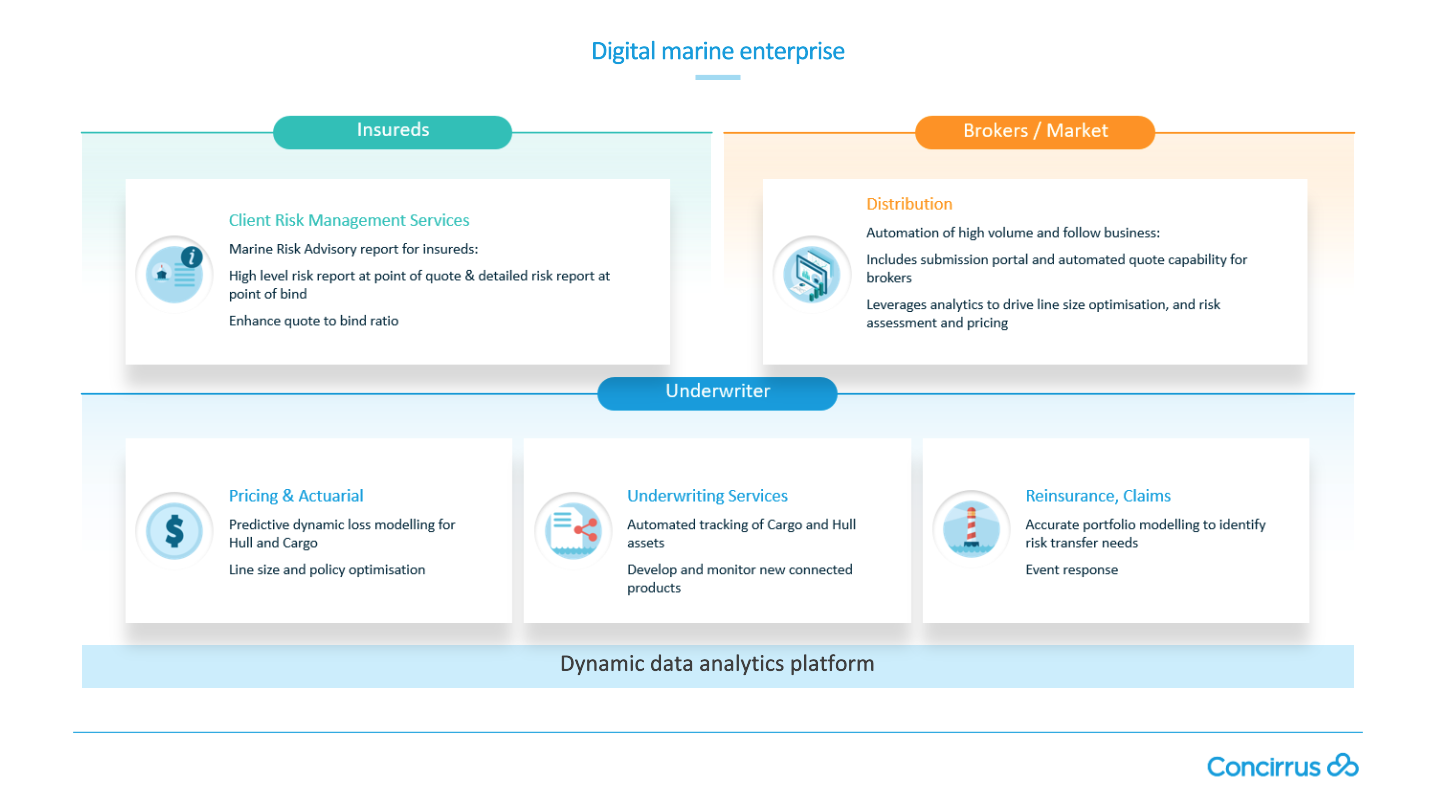

It all starts with data – this isn’t just your policy data or claims and exposure data, it’s all data related to the risk. Whether this is cargo trade data, hull risk data, traditional vessel information, real-time weather data, satellite imagery or vessel movement positioning. It is now possible to bring all this data together to help to better inform underwriting decisions.

The challenge is these datasets contain in the region of 500-600 billion rows and trillions of data points, which is too much to store within an organisation. A platform capable of processing this data and information quickly and effectively is therefore required.

The next thing you need is a dynamic modelling capability that uses machine learning concepts to drive insights from the data, promptly. This provides new insights to parts of the organisation that need them, supporting use cases and decision making across the enterprise.

Digital assets help in the adoption of such infrastructure. Digital assets are pieces of software that can be linked across technologies that provide specific functionality. Once these foundations are in place, three tiers of value become accessible.

What value comes from such investment?

If you have a dynamic pricing capability assessing all risks then you can completely automate the pricing of low-value high volume transactions. This is done by combining data models and digital assets to drive significant operational efficiency. Companies adopting this approach have a target expense ratio of around 8%, which is a dramatic improvement when compared to typical operations. Data platform modelling and digital assets can also be used by Underwriters in decision making. In an increasingly dynamic and predictive world, Underwriters need to ask more questions. Sometimes, the answer to those questions may not be obvious. Underwriters need quick access to rich insight to leverage such understanding with their experience to make the most suitable decision. This directly impacts loss ratios.

Digital assets can be used to extend the application of this intelligence beyond internal use, allowing for the development of new products and services such as advanced risk management reports.

Pricing and Actuarial

Data and behavioural analytics can be used to predict an expected loss based on risk score. Once you have this you can look at your portfolio and identify profitable and unprofitable segments, allowing you to act accordingly. Our work with customers has identified available loss ratio improvements of up to 20%. With this in place, Underwriters can focus on what matters. Segmentation and optimisation opportunities that arise from applying this perspective at the portfolio level can have a big impact.

Further opportunities from automation

Automating a big portion of your book allows experts to focus their time on areas of business that add the most value. A reporting tool can draw from pricing capabilities, which when combined with a quote to bind operating model, can immediately add value by differentiating a company’s services from the competition. The opportunity is bolstered through the addition of submissions or digital placement technologies.

Mark shared a case study comparing two vessels that on the surface looked identical using traditional rating factors. However, adding new behavioural datasets revealed two very different risk profiles. The impact of a limited view of risk on pricing and loss ratios can be significant. Access the case study here.

Machine learning can also lead to revolutionary insight into cargo exposure. Insights can be drawn based on an Insured’s name, revealing the number of shipments per day, consignment level and every port that shipments move through. An example of such insight is available here. If applied to risk modelling technologies, a composite view of hull/machinery and cargo risk across that entire route in real-time can be achieved. This gives Underwriters the ability to ask questions surrounding the data related to any risk they see quickly and effectively.

Innovation and business selection

The latest innovation from Concirrus includes an automated submissions capability within Quest Marine. Covid-19 has increased the use of electronic submissions methods such as email, and with a hardening market, Brokers are adding more Underwriters to each submission. This has led to an overwhelming number of submissions to assess per Underwriter. Concirrus’ submissions module addresses this challenge.

Email submissions are automatically ingested into the Quest Marine platform, augmented with risk profile data and priced. This allows Underwriters to quickly determine how new business fits their current risk appetite. Integration with Quest Marine makes the transition from receipt of email submissions to written policies seamless.

By linking a core predictive modelling capability that changes your view of risk to other areas of risk assessment, operations completely transform. Pricing technologies translate from managing loss ratios, to directing risk mitigation efforts, and then business selection.

Revenue Expansion - Client Risk Management Services

We have seen examples of this in cyber and property.

Over time data and modelling services have taken the form of risk consulting practices and in some cases data products from the larger (Re)Insurers. This typically overlays a modelling and data capability with a reporting visualisation tool. The same can be done in marine.

We’ve discussed behavioural models, the ability to automate submissions, and reporting tools. Extending revenue expansion use cases, including the application of a visualisation tool, is fairly simple and the beauty of a comprehensive platform is that there’s a whole range of directions adopters can take.

With technology comes opportunity – what does all this mean?

We spoke to our customers about their experience with lots of different POC’s. We also looked at other technologies within the market and what this could mean ahead of the coming year.

There are a host of possibilities for both cost savings and new revenue development associated with technology and risk modelling. We’ve included a selection below:

Potential savings

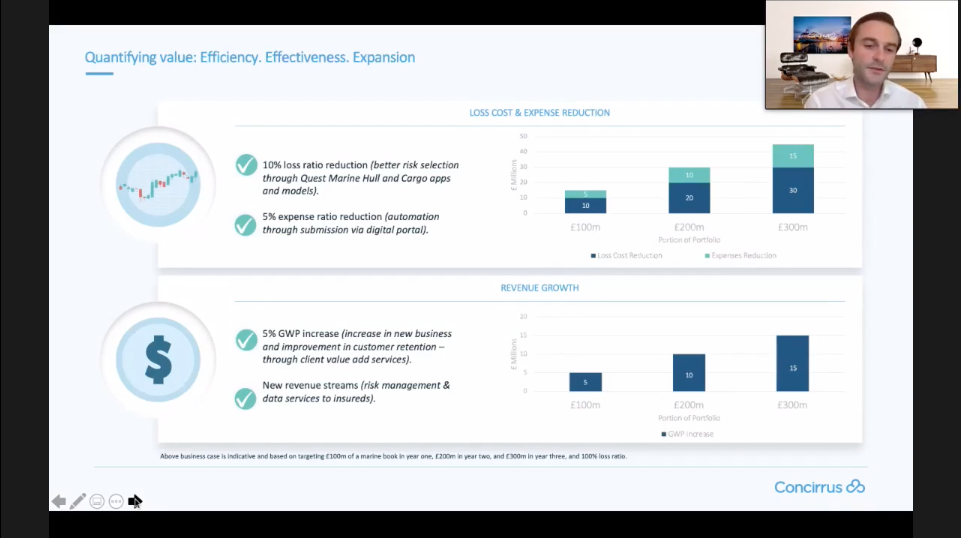

- Line size optimisation – in our experience can drive improvements of up to 20% in loss ratios

- Automating submissions – we believe could deliver reductions in expense ratios of up to 5%

New revenue opportunities

- Risk mitigation and loss prevention reports – providing actionable insight for your customer to help them reduce risk.

- Consultancy services – some customers may value your expert guidance in improving processes to mitigate risk.

- Connected policies – identify new flexible products and services for your clients to improve cover.

We’ve seen first-hand the impact of providing greater insights and supports in both quote to bind ratios and client retention.

The market has adapted to remote working at a rapid rate. The sum of digital initiatives being adopted across the market concerning product, placement and pricing shows clear movement in one direction.

As we look forward to the year ahead, we should continue to be shaken, we should continue to have the courage to push the boundaries. If we link these technologies together and start to think about not only the usage of those technologies internally, but how they can be extended to effect changes in our trading relationships, we have a fantastic opportunity to shape a new virtual insurance trading marketplace.

Learn more about Quest Marine here.

Download our blueprint report below.